A Guide to the Mortgage Interest Deduction

When you have a mortgage, there’s a deduction you can take on your taxes for the interest you pay on your first $1 million of debt. If you’re a homeowner who bought your home after December 15, 2017, you can deduct interest on the first $750,000 of your mortgage. If you are going to claim a mortgage interest deduction, you have to itemize your tax return.

read more

Fixed Loan? Hybrid? What’s the Difference?

It’s pretty much a fact that there are more home loan choices than you might think. Yeah, there are two basic types of mortgages, a fixed and an adjustable, but the choosing only starts there. With a fixed rate loan, it’s fairly easy to understand. The rate stays fixed throughout the life of the loan. The only differences in fixed rates are the loan terms. Most borrowers who select the fixed route take the 30 year term. But there are other terms as well.

read more

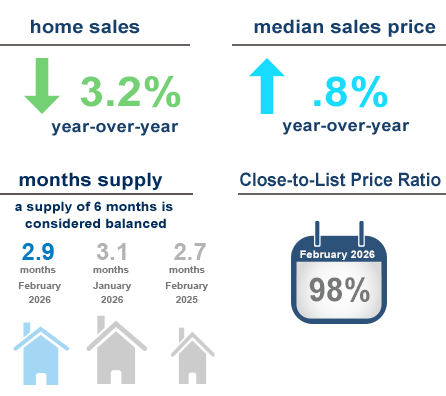

RE/MAX National Housing Report

February Listings Sell Faster Ahead of Spring, Inventory Holds Steady

read the full report

How to Tell How Much You Can Borrow

How much can you afford to borrow when getting ready to buy a home? That depends upon several factors, some more important than others. Affordability is generally determined by your monthly payment. Your monthly payment is affected by current market rates and the size of your home loan. In addition, the length of your loan will also affect the monthly payment. Shorter term loans for example may have a slightly lower rate but because the loan is squished into a 10 year term compared to the more common 30 year loan, the payment will be higher.

read more

An Insider’s Look at the Reality of Home Staging

When it comes to home staging, there are typically two buyer camps: The first thinks it’s a waste of money and doesn’t want to pay more to potentially make their home more attractive to buyers—even if their real estate agent says they’ll make it up (and then some). The second realizes the value and is willing to make that smart investment.

read more

Corvallis Market Conditions

Shape of the Current Market: Winter 2026

February Real Estate Roundup

"For the first time in three and a half years, the 30-year fixed-rate mortgage dropped into the 5% range, falling even lower than last week's milestone. This rate, combined with the improving availability of homes for sale, is meaningful and will drive more potential buyers into the market for spring homebuying season."

learn more